Nowadays, it is common for companies to encounter financial

difficulties or downturns that result in losses. Thus, understanding the tax treatment of business losses is essential for effective tax management and prudent budget planning to maximize potential benefits. This article provides an in-depth understanding of how companies should handle business losses from a tax perspective.

If the allowable expenses exceed the gross income of a particular business source in a particular year of assessment (YA), the resulting loss will represent a “current year business loss” (CYBL). The CYBL can be set off against income from all sources in the current year of assessment. However, if there is insufficient aggregate income in the current year of assessment, any excess CYBL will be carried forward and set off against aggregate statutory business

income in the following year of assessment.

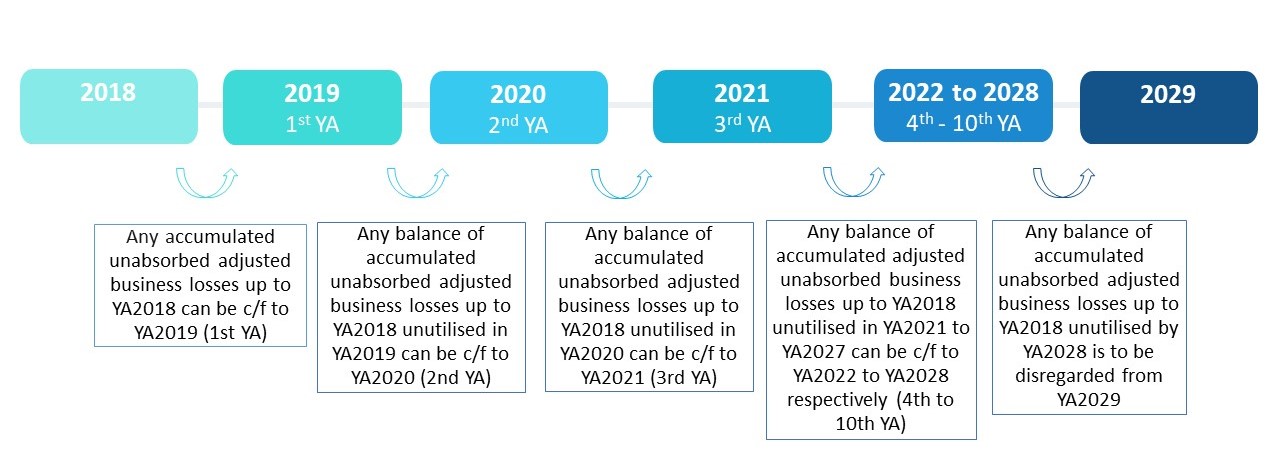

There has been an update regarding the time limit to carry forward unabsorbed business losses. Previously, businesses could only carry forward CYBL for a maximum period of 7 consecutive years of assessment. Any unutilised balances after that 7 consecutive years of

assessment period would be disregarded and permanently lost. However, as of YA 2019, the time limit for companies to carry forward the unabsorbed business loss has been extended for a period of 10 consecutive years of assessment. The primary purpose of the changes is to support the recovery of businesses that incurred losses due to the COVID-19 pandemic.

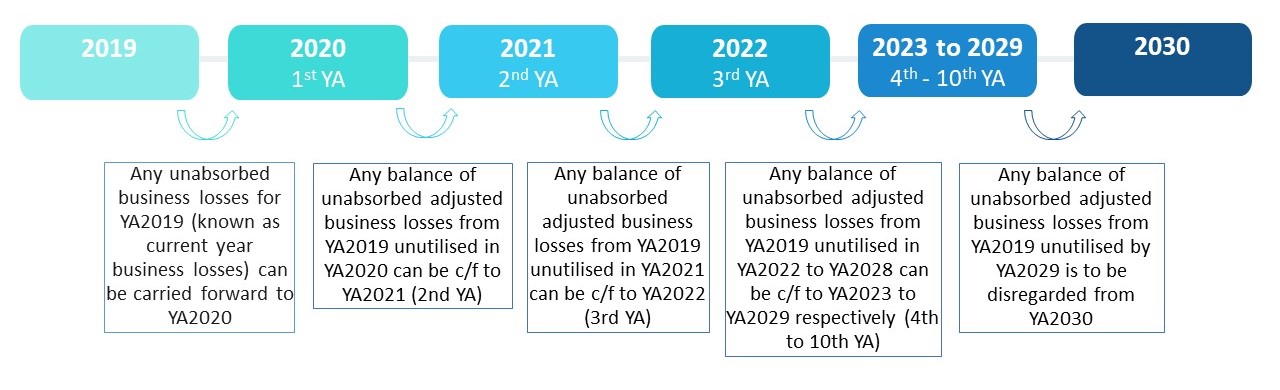

As illustrated in the table below, if a company has adjusted business loss in YA 2019, the unabsorbed business loss can be carried forward and utilised from YA 2020 to YA 2029. Any remaining unutilized business loss balance will be disregarded from YA 2030.