Are Businesses Still Facing Challenges in e-Invoicing Implementation? |

As we enter September, the second month of Phase 1 of the mandatory implementation of e-Invoicing, which began on 1 August 2024, are businesses still finding themselves in a critical phase of adapting to the new system? Are many still working through technical

integration issues, training staff, and adjusting internal workflows to align with the new requirements? Are businesses still facing challenges in implementing e-Invoicing, including

difficulties with software compatibility, managing large volumes of transactions, ensuring all transactions are handled correctly, and still navigating the new process while continuing to meet daily operational demands? In this article, let’s recap how businesses can utilise the temporary relaxation offered by the Inland Revenue Board of Malaysia (IRBM) to ease their transition into full e-Invoicing compliance. Recap: 6-Month Relaxation Period for

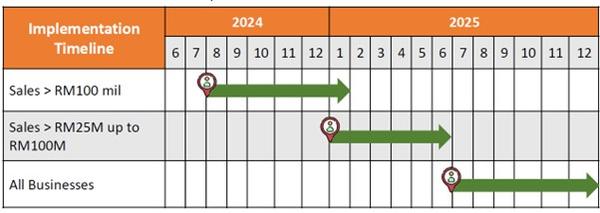

All Businesses The IRBM has announced flexibility for businesses to issue consolidated e-Invoices for six months starting from the mandatory e-Invoice implementation date for each phase as follows:- This relaxation period is provided to give businesses extra time to fully comply with the e-Invoicing requirements. During this period, businesses are permitted to issue consolidated e-Invoices for all types of transactions, including self-billed e-Invoices. This allows

businesses to group multiple transactions together and submit a consolidated e-Invoice, rather than issuing individual e-Invoices for each transaction. Important Considerations - This is a temporary measure

The implementation of e-Invoicing has not been delayed. The flexibility offered

by the IRBM is temporary, providing businesses with a six-month window to adapt. Consolidated e-Invoices must be submitted to the IRBM within 7 days after the end of each month. Failure to do so may result in penalties.

- Customer’s request for e-Invoices

During this relaxation period, businesses are not required to issue e-invoices individually for each transaction, even if a customer requests one. However, customers must still

receive a regular invoice, bill, or receipt for their purchases. Businesses should continue operating with their current invoicing system as usual during this transition period by issuing regular invoices, bills, or receipts and later consolidating all transactions on a monthly basis.

- Consolidation of e-invoices for all industries

All industries, including automotive, aviation, construction, etc., are now permitted to issue

consolidated e-invoices during this relaxation period. Additionally, this relaxation also applies to all circumstances requiring self-billed e-invoices, such as the importation of goods and services. This flexibility to issue consolidated e-Invoices is expected to significantly ease the transition for all sectors, ensuring a smoother path toward full e-invoicing compliance.

- Flexibility of Description for Product or Service

During

this relaxation period, the IRBM allows businesses greater flexibility to fill in any information or details in the “Description of Product or Service” field without restricting to fill in the receipt / statement / bill reference numbers.

- Penalties for non-compliance

During this six-month relaxation period, as long as taxpayers comply with the consolidated e-Invoice requirements, the IRBM will not

undertake any prosecution action under Section 120 of the Income Tax Act 1967.

The key to navigating this period is staying proactive, keeping detailed records, and submitting consolidated e-invoices in a timely manner to avoid penalties. By understanding these important updates, businesses can

ease their transition and ensure a smoother adoption of the e-Invoicing system. |

Subscribe to YYC taxPOD and unlock decades of tax-saving knowledge at your fingertips. Visit https://taxpod.com.my/taxknowledge

now! All Rights Reserved. All material in this presentation ("content") is the property of YYC taxPOD or the credited content provider. Without permission, you may not copy, reproduce, distribute, publish, display, perform, modify, create derivative works, transmit, or exploit this content in any way.

Distribution of any part of this content over any network is prohibited. For permission to use content from YYC taxPOD's materials, please contact learn@taxpod.my. |

|

|

|