6% or 8%? Get to Know The Latest F&B Industry Service Tax!

Published: Fri, 04/12/24

Service Tax Changes in

Malaysia's F&B

Industry

Recently, the Royal Malaysian Customs Department (RMCD) has made significant

adjustments to its service tax regulations, one of which is increasing the tax rate from the previous 6% to a new rate of 8%. Although the tax rates for certain industries such as the food and beverage (F&B) industry will preserve the existing tax rates of 6%, the move has still had an impact. Before delving into the specifics, let's first understand the concept of service tax in the F&B industry.

Service tax is a consumption tax levied on the prescribed services known as 'taxable services’. Specifically, the provision of prepared or served food and drinks is classified as a taxable service under Group B, First Schedule, Service Tax Regulations 2018. According

to the regulations, F&B operators who have a total turnover of RM1,500,000 for a period of 12-month shall be registered under the Service Tax Act 2018 and charge service tax on the provision of taxable services to their customers.

Following that introduction, we will now cover several service tax changes that are relevant to F&B industry. First of all, most businesses may find the 6% service tax rate for the F&B industry confusing. As we all know, while the tax rate for the F&B industry remains at 6%, the tax rate for other service industries has been increased to 8%. Therefore, assuming that

the F&B operators provide both F&B services and other services that are subject to an 8% tax rate, how should they determine which tax rate to apply?

According to the latest service tax

regulations, in cases where F&B operators offer other taxable services, the rate may not necessarily be fixed at 6%. If a Group B registered person offers a variety of taxable services, the service tax rates are determined based on the specific type of taxable service provided, rather than the primary service. However, if these taxable services are bundled together as a package, the service tax rate is determined based on the taxable service’s Group.

For instance, if a restaurant registered under Group B (i.e., F&B) provides both F&B along with management services, it should charge an 8% service tax for the provision of management services, despite being a

registered person under Group B.

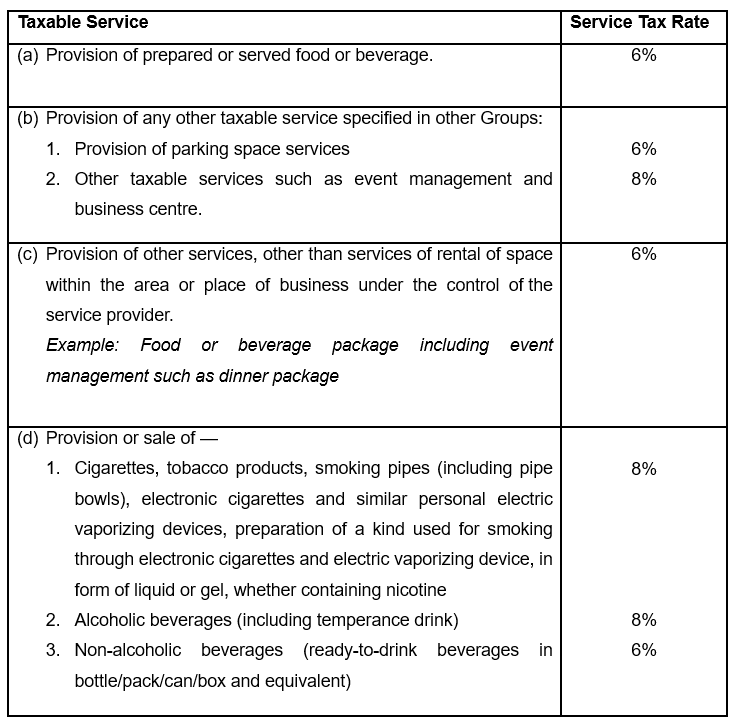

Furthermore, the RMCD has also issued a list detailing the prescribed service tax rates for registered persons under Group B who provide various taxable

services. Businesses can use the list as a reference and apply the appropriate tax rate according to the services they provide.

Moreover, the determination of tax rates for the following services provided by registered persons in Groups A, B, C, D, and E is at the specified rates as follows:

Alcoholic beverages provided in a F&B package such as buffet or banquet, are subject to a service tax rate of 6%;

Other service charges provided for the

provision of F&B, such as corkage fees, are subject to a service tax rate of 8%;

The provision or sale of snacks, fruits, and equivalent is not subject to service tax; and

Service charge is not subject to service tax.

Are you interested in learning more about the service tax changes announced by the RMCD recently?

Subscribe to TaxPOD now to access decades of tax-saving knowledge at your convenience, anytime and anywhere. Visit https://taxpod.com.my/taxknowledgenow!