Definition of Leave Passage

Pursuant to Public Ruling 1/2003 & Addendum to Public Ruling 1/2003, "Leave Passage" means travelling during a period of absence or vacation from duty or employment. If the cost incurred by the employer to the employee includes cost of air fares, food, accommodation, souvenirs and travel transportation, only amount relating to cost of fares is treated as leave passage cost.

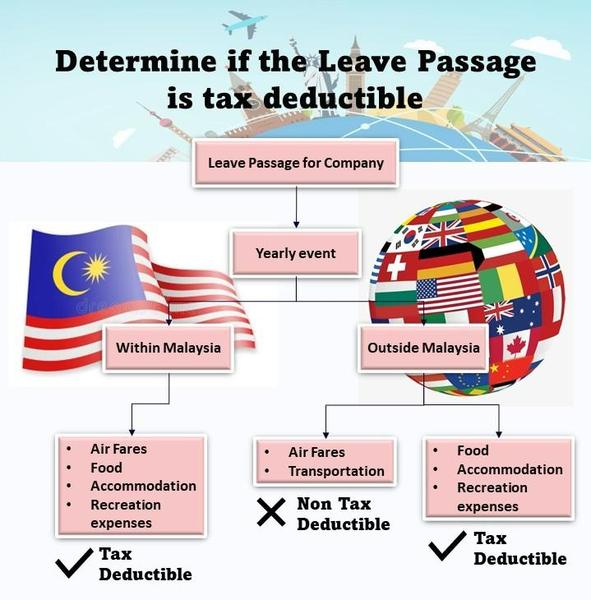

Local Leave Passage

Leave passage incurred by an employer to facilitate a yearly event within Malaysia which involves the employer, employee and immediate family members of that employee is categorised as entertainment expense specified under Proviso (viii) of Paragraph 39(1)(l), ITA 1967. Thus, it is wholly

allowable. In addition, cost of meals and accommodation spent on employees are also allowable deduction under aforesaid proviso.

Non - Local Leave Passage

Non-local leave passage given by employers to employees (including director of a company) in relation to air fares is not eligible for tax deduction.

However, expenses incurred on meals and accommodation spent on employees are allowed a deduction under proviso (i) of subparagraph 39(1)(l), ITA 1967.

Note:

Leave

passage benefit provided to partners or sole proprietors will not qualify for a tax deduction.