Transfer pricing generally refers to the

intercompany pricing arrangements for the transfer of goods, services, and intangibles between related or associated parties. In an ideal scenario, the transfer price should be the same as the prevailing market price. However, business transactions between associated parties may not always reflect the dynamics of market forces.

In view of this, the Malaysian Inland Revenue Board (HASiL, abbreviated as IRB from here onward) has updated the Transfer Pricing Guidelines 2012 (with effect from 15 July 2017) to take into account new legislations proposed in the 2020 Budget announcement.

The Arm’s Length Principle

Malaysia follows what we call the arm’s length principle to determine transfer prices for transactions between related parties. Prices are only deemed acceptable when they are at arm’s length, which involves comparing controlled and uncontrolled transactions based on factors such as prices, margins, and division of profits. The arm’s length principle is internationally accepted as the preferred basis for determining the transfer price of a transaction between

associated persons.

Controlled Transactions and Associate Persons

Pursuant to Section 139 of the Income Tax Act 1967:

“Control” refers to both direct and indirect control.

“Associate” refers to:

(a) Persons in any of the following relationships to that person, such as husband or wife, parent or remoter forebear, child or remoter issue, brother, sister and partner;

(b) Trustee or trustees of a settlement in

relation to which that person is, or any such relative of his as mentioned in paragraph (a);

(c) Where the person is interested in any shares or obligations of a company.

The guidelines are applicable on controlled transactions for the acquisition or supply of property or services between associated persons, where at least one person is assessable or chargeable to tax in Malaysia.

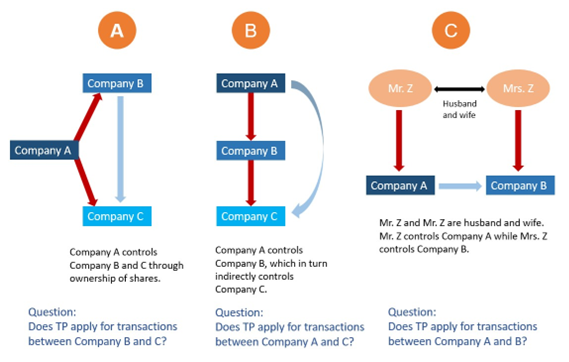

Consider Scenarios A, B, and C: