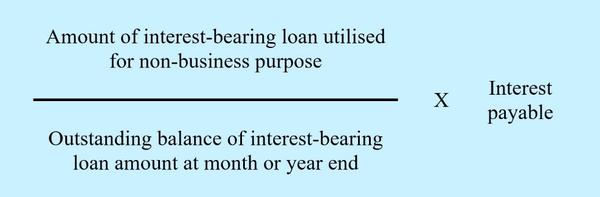

If the total cost of

investments and loans which are financed directly or indirectly from the borrowed money does not exceed RM500,000, the s.33(2) interest restriction will be computed based on the end-of-year balance.

However, if the total cost of investments and loans which are financed directly or indirectly from the borrowed money exceeds RM500,000, or there are no investments and loans at the end of the financial year because the investments and loans that are financed directly or indirectly by the borrowed money have been sold, transferred, or repaid during the year, the s.33(2) interest restriction will be applied strictly based on monthly

balances and the relevant information should be kept by the taxpayer for tax audit purposes.

Non-Application of Interest Restriction

The s.33(2) interest restriction is not applicable if the interest on borrowed money charged to the business accounts does not exceed RM10,000 for companies and RM6,000 for individuals and others.

If the interest on borrowed money charged to the business accounts exceeds RM10,000 for companies and RM6,000 for individuals and others, then the s.33(2) interest restriction should be applied. However, the interest disallowed for business purposes as a result

of applying s.33(2) can be offset against income from investments or loans, whichever is applicable.