Is the Withholding Tax borne by payer tax deductible?

What if Withholding Tax Is Borne by

Payer?

We now know that withholding tax (WHT) applies

when we make payments to non-resident individuals or bodies. The WHT amount to be remitted to the Malaysian Inland Revenue Board (HASiL) is calculated by way of multiplying the gross payment amount with the corresponding WHT rate depending on the payment type. Do note that preferential tax rates may apply if the payee’s country has entered into a Double Tax Agreement (DTA) with our country.

In an ideal situation, the WHT would be borne by the payee and deducted from the fee paid to them. However, what happens if the payee refuses to bear the WHT? The payer would then be unable to deduct the amount to be remitted to the Inland Revenue Board from the payment made to the non-resident payee.

When this happens, the payer will have to bear the WHT.

Facts

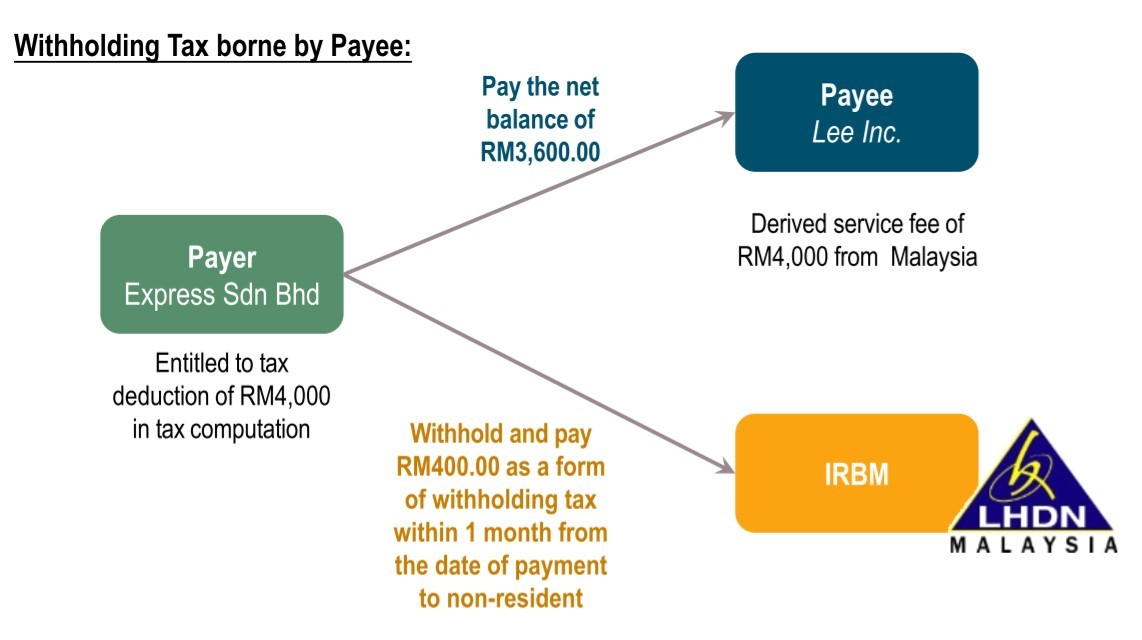

Express Sdn. Bhd. (the payer) engaged Lee Inc. (the payee) from America to craft an advertisement video for their company in 2021. The service fee amounted to RM4,000.

An ideal situation would look like this:

Express Sdn. Bhd. would pay the net balance of RM3,600 to Lee Inc. and remit RM400 to the Inland Revenue Board one month from the date they made the payment to Lee Inc.

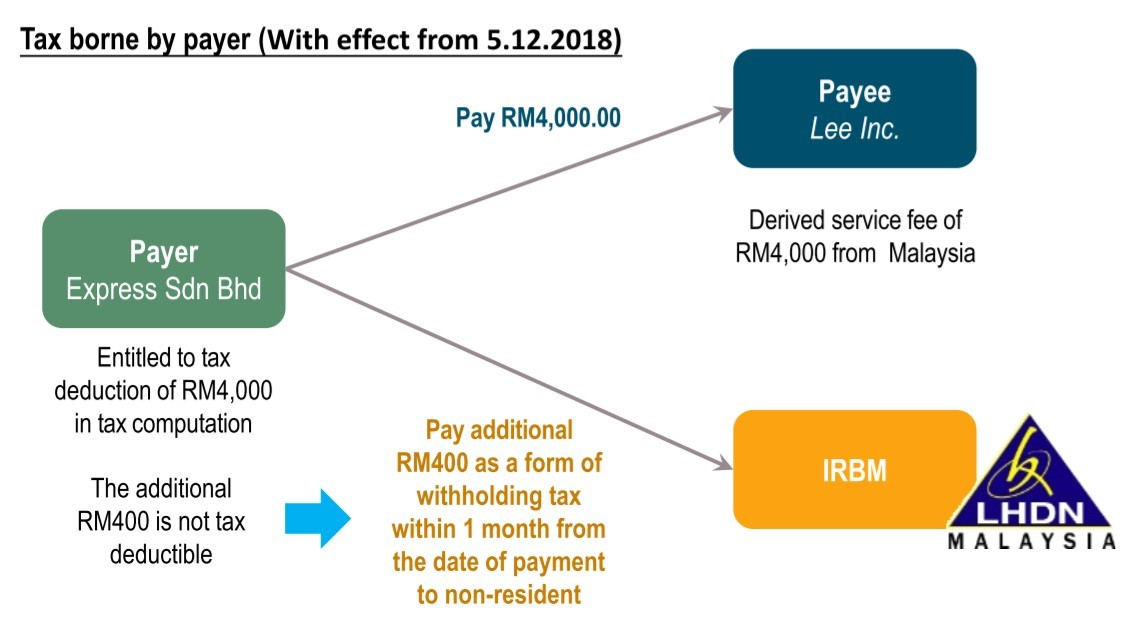

Now, imagine if Lee Inc. refuses to bear the WHT and demands Express Sdn. Bhd. to make the full payment of RM4,000. What happens then is that Express Sdn. Bhd. will have to be the party to bear the WHT on top of paying the full amount of the service fee to Lee Inc.

It can be seen that if the WHT is borne by

Express Sdn. Bhd., they would need to fork out an additional RM400 in addition to paying Lee Inc. the full amount of RM4,000. Instead of just paying RM4,000, Express Sdn. Bhd. will need to pay RM4,400 in total.

Even when the WHT cannot be deducted from the payee, it is still important to pay it. That is because if the WHT is not paid, the service fee that is charged will not be tax-deductible in the payer’s tax computation.

In Express Sdn. Bhd.’s case, they would be entitled to a tax deduction of RM4,000 for the service fee paid to Lee Inc. As long as the service provided is in relation to the payer’s business, it is tax-deductible. Then, what about the additional RM400 of WHT? Would that be tax-deductible together with the service fee? The answer to that is “No.” It is an extra cost that the payer is not supposed to pay on their own and it is not incurred in

relation to their business. The payer is just paying it to comply with the WHT rule.

Not sure which is the right form for you and how to fill it out? Decades of tax-saving knowledge will be available to you right at your fingertips.

Sign up for TaxPODto find out more and get access to decades of tax-saving knowledge.